Friday 20th January 2023

I recently read a write-up on eXp World Holding (NasdaqGM:EXPI), an online real-estate brokerage firm in the US on Value Investors’ Club, here.

The “pyramid scheme” nature of acquiring and retaining real-estate agents, combined with the revenue-share nature of paying them, may well provide a durable moat for this business, enabling a consolidation of US housing transactions. With 50k agents currently (6% of agents in the US) and ambitions to reach 250k, there may well be room for growth ahead.

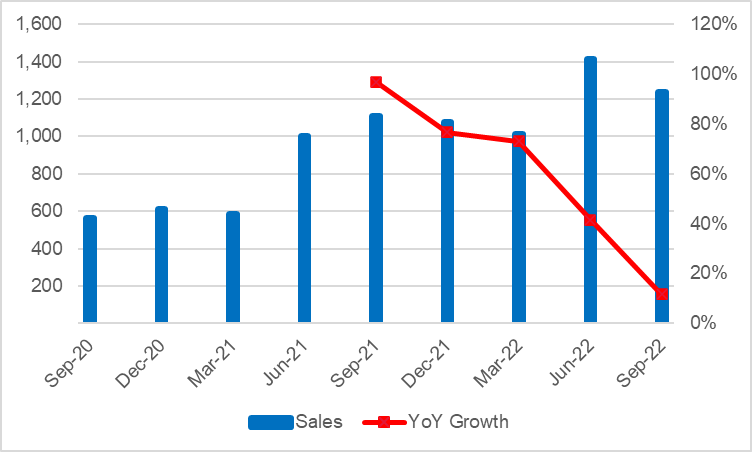

With TTM revenue growth slowing (from 97% in Sep-21 to 12% in Sep-22), the 50x TTM FCF multiple looks ripe for de-rating.

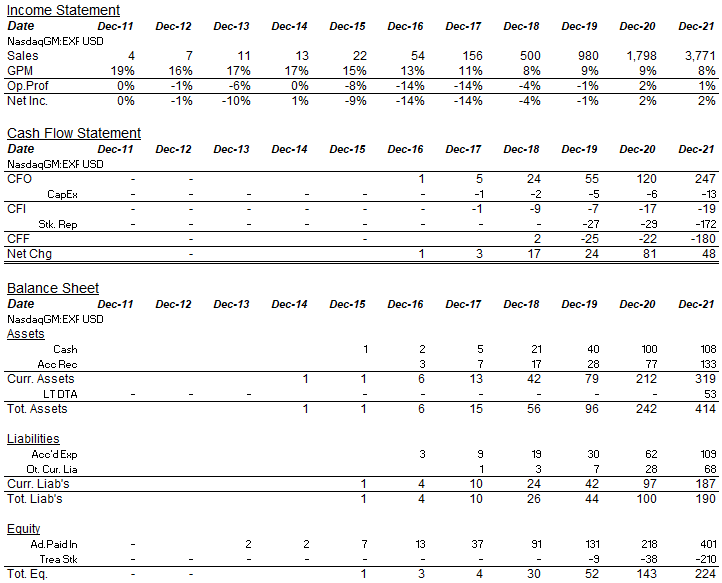

- Summary Financials

- Things I like about EXPI

- Things that concern me about EXPI

- Might be good-Might be bad

- Things I don’t know the answer to yet

Summary Financials

Things I like about EXPI

- eXp gives all agents their own websites, CRM and health insurance (through Clear Water, not many other brokerages offer this). This should help in retaining the agents EXPI has acquired in the past.

- Agents get a share of revenue generated by agents they bring to the platform into perpetuity, funded by EXPI.

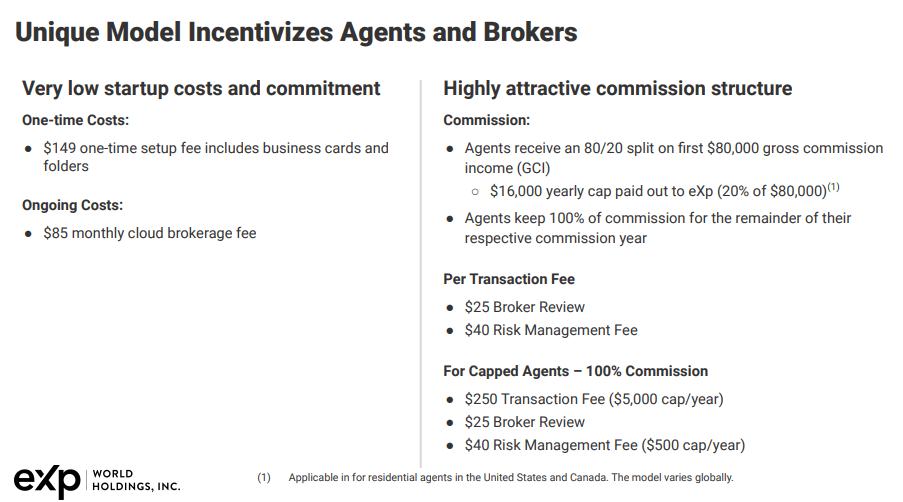

- The attractive economics of the model for agents should help EXPI organically bring agents onto their platform, reducing their reliability on agents bringing in sponsored agents (with lower margins for EXPI) (Exhibit 1)

Exhibit 1: EXPI offers agents 80%+ of the brokerage revenue made on closing a sale

Source: Company presentation, Q2 ’22

Things that concern me about EXPI

- Valuation: At $2bn, the company is currently valued at 52x earnings from Sep-21 to Sep-22 (Q4’22 numbers not yet released), and 60x free-cash-flow (Net Income plus depreciation and amortisation, less capex) over the same period. Given the year-on-year sales growth over that period has declined from 97% to 12%, the risk of a de-rating seem high. (Exhibit 2). With US house prices now declining in several cities, and mortgage rates high relative to disposable incomes, the risk is exacerbated.

Exhibit 2: The rapid decline in growth makes a stock de-rating likely

Source: Company filings

2. EXPI’s share of commissions is limited to $16,000. That means if house prices grow (as they have historically at 5.5% CAGR) then EXPI will likely see its gross margins contract into single digits.

Might be good-Might be bad

- As the business grows (more agents on the platform) the benefit to new joiners does not improve in the way of a social network. In fact, because of the “no geographical limits” imposed on the cities agents can operate in, it might well be the case that agents and all their sponsors split off into separate “pyramid” teams that compete with one another. Its unclear to me if this type of potential internal competition would be beneficial to EXPI overall or that it might damage the image of the broker to home buyers and sellers.

Things I don’t know the answer to yet

- EXPI closed around 500k homes in 2022. This compares to total homes sold in the US each year of about 5-6m. They currently operate in 20 countries and plan to be in 100 countries by 2031. There is a risk this ambition fuels reckless agent-acquisition costs as they look to break into new markets.