Investment Thesis

Double-digit growth in university students will likely continue to support increased demand for HMOs – homes of multiple occupation- in student cities. This combines with increased costs and regulations for HMO landlords, in addition with local council rules, limiting supply of student homes. Together these are likely to support continued 5%+ growth rates in student rents for the next few years.

In general, with student housing and HMOs typically located outside city centres, benefiting from steady demand from new streams of students each year, the higher yields can make them a good investment even if the overall property market dips.

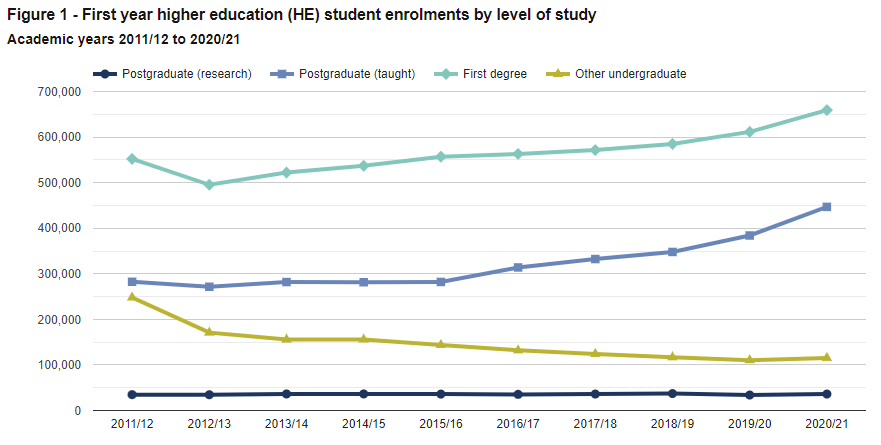

Growing student numbers increase demand

There has been an acceleration in undergraduate intake (Figure 1), this creates resilient demand:

Source: Higher Education Student Statistics: UK, 2020/21

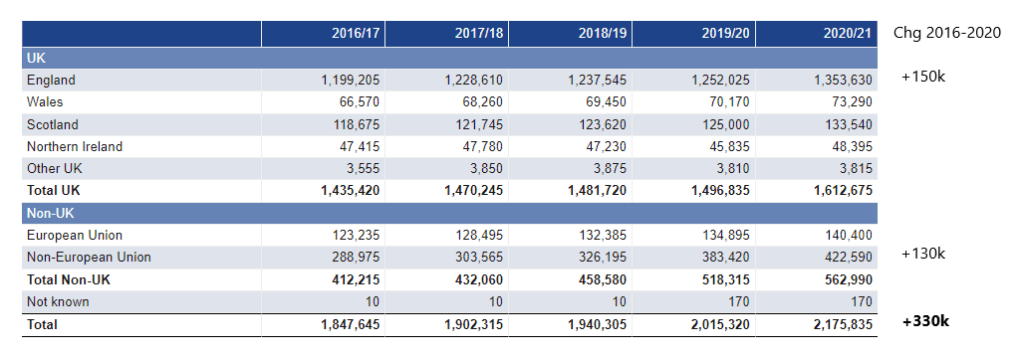

Student intake at English universities has increased every year since 2016. Of the 330k more students in 2020 relative to 2016, more than 80% came from England and Non-EU countries (mainly China, ~30%). This is significant because foreign students have to pay more for their education and therefore would presumably also be able to afford to pay more for their accommodation (Figure 2).

Figure 2: English and Non-EU students drive growth in university numbers

Source: Higher Education Student Statistics 2020/21

Exhibit 1: The percentage of UK 18-21 year olds going to university is increasing

Source: ONS

Exhibit 2: UK population of University age adults is set to increase

Source: ONS

Supply of student accommodation is unlikely to increase dramatically

There is a shortage of student housing in the UK. Currently, the UK has 700,000 rooms in purpose-built student blocks. About 370,000 of these were built by specialist student developers, such as Unite.

According to calculations by Cushman & Wakefield, there are about 2.4 students for every room in purpose-built student accommodation. But houses in multiple-occupation residential properties, preferred by students after their first year, are also under “massive pressure” having been left to pick up the excess demand.

In addition there is also legislation in place in certain councils that limits the number of student homes that can be built. Councils talk of their “responsibility” to ensure student housing does not adversely affect local residents.

The imbalance has led to double-digit annual growth in rental prices in some university towns. Nationally, Cushman estimated student private rents had risen 19.3 per cent, and university rents by 14.5 per cent, since 2016-17.

The worst affected cities include Durham, Manchester, Bristol, Glasgow and York.

This term, first years at the University of the West of England in Bristol were housed in Newport, more than half an hour away by train; those at Manchester Metropolitan University were offered halls in Liverpool, an hour away. Meanwhile, in Glasgow, students were told not to relocate to the city because housing could not be guaranteed.

Source: FT, “University expansion drive collides with UK student housing shortage”, Nov. 8, 2022

Listed provider of student housing, Unite, said they expect sales to grow at 4.5-5% partly as a result of these factors in addition to a reduction in supply from landlords operating HMOs – houses in multiple occupation.

“You then look at the HMO market, so student takes a market that’s got 1 million or so students in it. That market is actually declining as buy-to-let landlords are selling or not renting to students. Therefore, over the course of the next 2 to 3 years, we actually expect a net reduction in the total number of beds available for students to rent at university.”

Richard Smith, Unite Group CEO, Q3 2022 Earnings Call

Landlords operating HMOs have been hit by a confluence of headwinds of late:

- Regulations:

- HMO licenses must be applied for here

- Landlords must send the council an updated gas safety certificate every year

- Install and maintain smoke alarms

- Provide safety certificates for all electrical appliances when requested

- From 2025, all newly rented properties are likely to require an EPC rating of C or above. While the Bill has not yet been enacted, it states:

(a) all new tenancies must have an energy efficiency performance of at least EPC Band C from 31 December 2025; and

(b) all existing tenancies must be at least EPC Band C from 31 December 20 2028 where practical, cost-effective and affordable as defined under section 1(4).

Source: Minimum Energy Performance of Buildings (No. 2) Bill